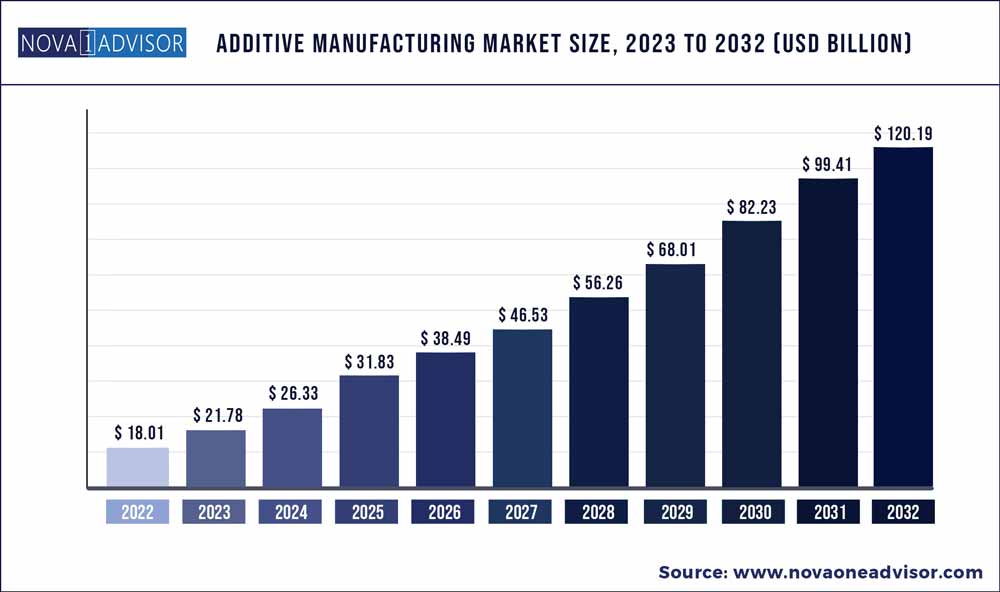

The global Additive Manufacturing market size was exhibited at USD 18.01 billion in 2022 and is projected to hit around USD 120.19 billion by 2032, growing at a CAGR of 20.9% during the forecast period 2023 to 2032.

Key Pointers:

Additive Manufacturing Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 21.78 Billion |

|

Market Size by 2032 |

USD 120.19 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 20.9% |

|

Base year |

2022 |

|

Forecast period |

2023 to 2032 |

|

Segments covered |

Component, printer type, technology, software, application, vertical, material, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central and South America; the Middle East and Africa |

|

Key companies profiled |

Stratasys, Ltd.; Materialise NV; EnvisionTec, Inc.; 3D Systems, Inc.; GE Additive; Autodesk Inc.; Made In Space; Canon Inc.; Voxeljet AG |

A total of 3.2 million units of 3D printers were shipped globally in 2022 and the unit shipments are expected to reach 22.5 million units by 2030. Factors such as the growing demand for prototyping applications from various industries and industry verticals, particularly healthcare, automotive, and aerospace & defense, and the aggressive research and development in 3D printing are expected to drive the growth of the market.

Additive Manufacturing (AM) is different from the subtractive method of production, which envisages grinding out unnecessary material from a block of material. The use of additive manufacturing in industrial applications usually refers to 3D printing. Additive manufacturing involves a layer-by-layer addition of material to form an object while referring to a three-dimensional file with the help of a 3D printer and 3D printer software. A suitable additive manufacturing technology is selected from the available set of technologies depending upon the application.

The deployment of additive manufacturing includes providing installation services, offering consultation solutions and customer support, and handling various aspects related to copyrights, licensing, and patenting. Additive manufacturing is helping manufacturers in prototyping, designing the structure and end products, modeling, and shortening the time to market. As a result, the production expenses have reduced considerably, and manufacturers are in a better position to offer products at reasonable prices. The adoption of 3D printers is expected to increase as a result of these benefits.

However, misconceptions among small- and medium-scale manufacturers about the prototyping processes are hindering the adoption of additive manufacturing. These manufacturers are deliberating before considering investments in prototyping as accountable investments rather than trying to realize the benefits of prototyping. The general notion is that prototyping is merely an expensive phase before manufacturing. Such perceptions and the looming lack of technical knowledge and standard process controls are expected to restrain the growth of the market.

The outbreak of the COVID-19 pandemic has taken a severe toll on the overall economy, and subsequently, the global market for additive manufacturing. The lockdowns and the restrictions on the movement of people and goods imposed by various governments worldwide as part of the efforts to arrest the spread of coronavirus typically disrupted the logistics and supply chain, triggered a shortage of labor, and affected the production of additive manufacturing printers. These lockdowns and restrictions particularly restrained the growth of the market during Q1/2020 and Q2/2020.

Printer Type Insights

The industrial 3D printer segment dominated the market in 2022 and accounted for a revenue share of more than 64%. Industrial 3D printers are being adopted extensively across various industries and industry verticals, including automotive, electronics, aerospace & defense, and healthcare, among others, for some of the common applications, such as prototyping, designing, and tooling. Given the extensive adoption of additive manufacturing for prototyping, designing, and tooling, the industrial 3D printer segment is expected to continue dominating the market over the forecast period.

Desktop 3D printers were initially limited to hobbyists and small enterprises. However, desktop 3D printers are increasingly being used for household and domestic purposes. Schools, educational institutes, and universities are also adopting desktop 3D printers for technical training and research purposes. Smaller businesses are typically adopting desktop 3D printers and diversifying their business operations to offer additive manufacturing and other related services. Hence, the demand for desktop printers is expected to rise significantly over the forecast period.

Technology Insights

The stereolithography segment dominated the market in 2022 and accounted for a revenue share of more than 9.4%. Stereolithography happens to be one of the oldest and most conventional printing technologies. Apart from ease of operations, there are several other advantages associated with stereolithography, which are encouraging the adoption of the technology. However, advances in technology and aggressive research & development activities being pursued by industry experts and researchers are opening opportunities for several other efficient and reliable technologies.

Apart from stereolithography, there are several other additive manufacturing technologies used in the market. They include fuse deposition modeling (FDM), direct metal laser sintering (DMLS), selective laser sintering (SLS), inkjet printing, polyjet printing, laser metal deposition, and electron beam melting (EBM), digital light processing (DLP), laminated object manufacturing, and others. While FDM is also adopted significantly; DLP, EBM, inkjet printing, and DMLS are also gaining significant traction as these technologies are applicable in specialized additive manufacturing processes.

Software Insights

The design software segment dominated the market in 2022 and accounted for a revenue share of more than 31.7%. The segment is also expected to continue dominating the market over the forecast period. Design software is used for constructing the designs of the object to be printed, particularly in the automotive, aerospace & defense, and construction & engineering industries. There are several advantages associated with design software. One of the advantages is the capability of design software to serve as a bridge between the object to be printed and the printer’s hardware.

Apart from design software, there are other different types of software used in the market. They include scanning software, printer software, and inspection software. The demand for scanning software is poised for significant growth over the forecast period in line with the growing trend of scanning objects and storing scanned documents. The ability to store the scanned images of the objects irrespective of their sizes and dimensions for 3-dimensional printing is expected to drive the demand for scanning software. The scanning software segment is expected to grow at the highest CAGR of 21.8% from 2023 to 2032.

Application Insights

The prototyping segment dominated the market in 2022 and accounted for a revenue share of more than 56.4%. The prototyping process is used extensively across several industries and industry verticals. Incumbents of the automotive and aerospace & defense industries particularly use prototyping to precisely design and develop parts, components, and complex systems. Prototyping allows manufacturers to achieve higher accuracy and develop reliable end products. Hence, the prototyping segment is expected to continue dominating the market over the forecast period.

Other applications considered as part of the study include tooling and functional parts. Functional parts include smaller joints and other metallic hardware required for connecting components. The accuracy and precise sizing of these functional parts are of paramount importance while developing machinery and systems. As a result, incumbents of several industries and industry verticals are putting a strong emphasis on designing and building functional parts with utmost precision. Hence, the functional parts segment is expected to grow at a significant CAGR of 21.4% from 2023 to 2032.

Vertical Insights

The automotive segment dominated the market in 2022 and accounted for a revenue share of more than 20.9%. Based on vertical, the market has been further segmented into industrial additive manufacturing and desktop additive manufacturing. The automotive segment falls under industrial additive manufacturing along with aerospace & defense and healthcare, among others. The healthcare segment is poised for significant growth in line with the growing adoption of additive manufacturing to develop artificial tissues and muscles replicating natural tissues for use in replacement surgeries.

The desktop additive manufacturing segment has been further segmented into educational purposes, fashion & jewelry, objects, dental, food, and others. The dental, fashion & jewelry, and food segments are anticipated to contribute significantly to the growth of the desktop additive manufacturing segment over the forecast period. The dental segment accounted for the largest revenue share in 2022 and is expected to continue dominating the segment over the forecast period. Additive manufacturing is also gaining traction in imitation jewelry, miniatures, art & craft, and clothing & apparel.

Component Insights

The hardware segment dominated the market in 2022 and accounted for a revenue share of more than 61.8%. The strong emphasis manufacturing entities continued to put on pursuing advanced manufacturing practices and rapid prototyping allowed the hardware segment to dominate the market. The hardware segment is poised for significant growth over the forecast period owing to various factors, such as rapid industrialization, the growing demand for consumer electronics products, the continued development of civil infrastructure, rapid urbanization, and optimized labor costs.

Based on component, the market has been further segmented into hardware, software, and services. Technology proliferation, the growing adoption of rapid manufacturing processes, such as rapid prototyping, and the widening application portfolio of additive manufacturing across various industries and industry verticals are expected to propel the demand for all the components associated with additive manufacturing. The technology allows layer-by-layer procedural manufacturing of three-dimensional objects that are connected through a system comprising applicable digital files.

Material Insights

The metal segment dominated the market in 2022 and accounted for a revenue share of more than 51%. Looking forward, the metal segment is anticipated to continue dominating the market and expand at the highest CAGR of more than 21.2% over the forecast period. Based on material, the market has been further segmented into polymer, metal, and ceramic. The polymer segment accounted for the second-largest revenue share in 2022. On the other hand, the ceramic segment is poised for significant growth over the forecast period.

Although additive manufacturing using ceramic is a relatively newer technique, the R&D initiatives market players are pursuing for AM technologies, such as FDM and inkjet printing, are driving the demand for ceramic AM. Opting for the AM methodology can allow manufacturers to produce complicated, delicate parts at greater ease and with high precision and accuracy. Moreover, enhanced material usage is also allowing manufacturers to reduce their production expenditures significantly. All these benefits and advantages associated with the technology are driving the adoption of AM.

Regional Insights

North America dominated the additive manufacturing market in 2022 and accounted for a revenue share of more than 35.9%. North America is home to developed economies, such as the U.S. and Canada. These economies are considered among the prominent and early adopters of the latest technologies. On the other hand, Europe emerged as the second-largest regional market. Europe happens to be the largest region in terms of geographical footprint. Europe is also home to several companies holding strong technological expertise in additive manufacturing.

Asia Pacific is poised for remarkable growth. The regional market is expected to grow at the highest CAGR over the forecast period. The growth of the regional market can be attributed particularly to the continued developments and upgrades being pursued by the incumbents of the manufacturing industry across the region. Asia Pacific is emerging as a manufacturing hub for the automotive, healthcare, and consumer electronics industries. Rapid urbanization is also expected to play a vital role in driving the adoption of three-dimensional printing across the region over the forecast period.

Some of the prominent players in the Additive Manufacturing Market include:

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2032. For this study, Nova one advisor, Inc. has segmented the global Additive Manufacturing market.

By Component

By Printer Type

By Technology

By Software

By Application

By Vertical

By Material

By Region

Additive Manufacturing Market