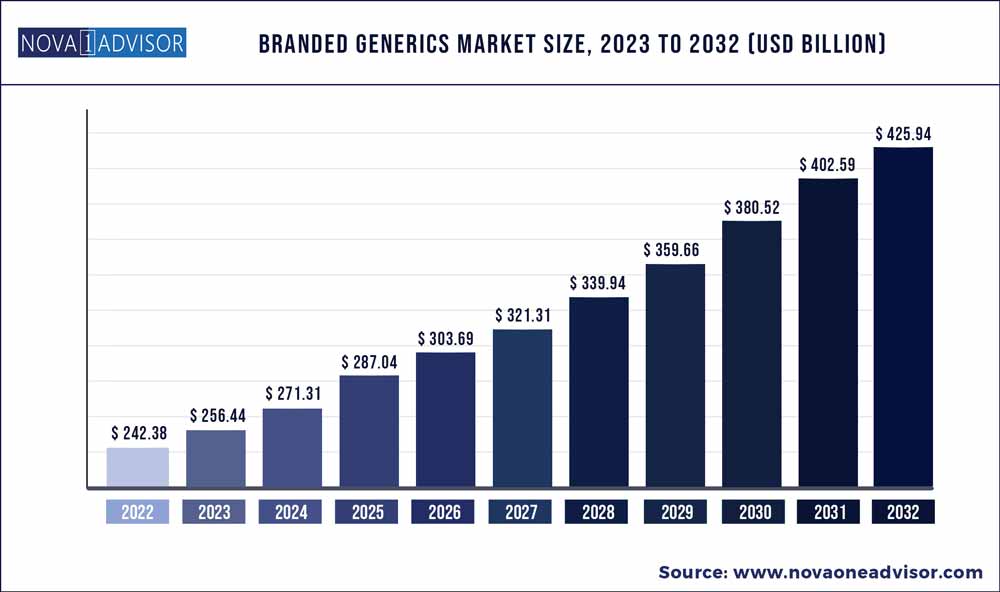

The global Branded Generics market size was exhibited at USD 242.38 billion in 2022 and is projected to hit around USD 425.94 billion by 2032, growing at a CAGR of 5.8% during the forecast period 2023 to 2032.

Key Pointers:

Branded Generics Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 256.44 Billion |

|

Market Size by 2032 |

USD 425.94 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 5.8% |

|

Base year |

2022 |

|

Forecast period |

2023 to 2032 |

|

Segments covered |

Drug class, application, route of administration, distribution channel, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central and South America; the Middle East and Africa |

|

Key companies profiled |

Teva Pharmaceutical Industries Ltd.; Lupin; Sanofi; Sun Pharmaceutical Industries, Ltd.; Dr. Reddy's Laboratories Ltd.; Endo International plc; GlaxoSmithKline plc; Pfizer Inc.; Apotex, Inc.; Viatris, Inc. |

Furthermore, the market is projected to expand at a CAGR of 5.8% from 2023 to 2032. Factors such as patent expiry of major products, the rising prevalence of chronic diseases, high penetration of generic products, and government initiatives to promote them for reducing the overall healthcare expenditure are among the primary growth drivers.

The patent expiry of branded products primarily fuels industry growth. Drugs, such as Revlimid and Alimta, may cost up to USD 500 a month, which affects the overall healthcare expenditure and affordability for patients suffering from chronic diseases. Eli Lilly & Company’s Alimta is expected to lose its patent protection by May 2022. This expiry of product patents creates opportunities for generics and biosimilar manufacturers.

However, over the past few years, the trend of ANDA approvals for generic drugs had been steadily decreased. It can be observed that the number of ANDA approvals decreased from 1,014 in 2019 to 948 in 2020 and further declined to 776 in 2021. Such factors could slow down industry growth in the coming years.

The growing burden of infectious & non-infectious diseases, coupled with the rising geriatric population, which is more susceptible to chronic diseases such as diabetes, hypertension, and obesity, is expected to positively impact the industry growth. According to an NCBI article, there were 537 million patients suffering from diabetes in 2021 globally.

The COVID-19 pandemic moderately impacted the branded generics space. Due to lockdown situations and stringent government regulations to curb the pandemic, a slowdown and disruption in the supply of pharmaceuticals had been observed in the initial phase of the pandemic. In addition, regulatory operations also affected reimbursement decisions and approvals of new products in the space. However, the market regained its pace by the end of 2020 in most countries.

Companies are introducing novel products to strengthen their product portfolio. In March 2022, Viatris, Inc. received the U.S. FDA’s approval for Breyna, the first generic version of AstraZeneca's Symbicort, intended for the treatment of COPD. Moreover, in February 2019, Mylan N.V. introduced the first generic version of ADVAIR DISKUS (fluticasone propionate and salmeterol inhalation powder) under the brand Wixela Inhub for the treatment of patients with Chronic Obstructive Pulmonary Disease (COPD) or asthma. This branded generic was claimed to be 70% cheaper than the originator product.

Drug Class Insights

The anti-hypertensive segment dominated the marketspace in 2022 with a revenue share of 16.19%, due to the rising ANDA approvals and product launches over the past few years. For instance, in June 2019, Teva Pharmaceuticals Industries Ltd. and Hikma Pharmaceuticals PLC introduced the generic version of Tracleer in the U.S.

The hormones segment is anticipated to expand at a high growth rate through the projection period, due to rising investments to develop value-added or complex generics. An increasingly sedentary lifestyle is driving the prevalence of various metabolic disorders. Hormonal imbalance is a growing concern in a majority of the countries. These disorders include thyroid and sex hormone imbalance.

Application Insights

The oncology segment is projected to advance at the fastest CAGR of 6.3% by 2032, due to the patent expiry of key drugs in this area. The increasing disease burden may also contribute to market growth. According to WCRF International, in 2020, there were an estimated 18.1 million cancer cases globally, of which 8.8 million cases were among women and 9.3 million cases were among men.

The gastrointestinal diseases segment is projected to advance at a moderate CAGR during the forecast period, due to the growing demand for related products. An NCBI article suggests that around 119 million prescription proton pump inhibitors were sold globally in 2020.

Route of Administration Insights

The oral segment accounted for the largest revenue share of 60.19% in 2022 in the branded generics market, due to several advantages of oral dosage over other forms, such as ease of administration and no nursing requirements, thus leading to higher patient acceptability and compliance.

On the other hand, the parenteral segment is expected to advance at the fastest CAGR of 6.11% during the forecast period. An increase in the prevalence of target diseases, such as cancer, hepatitis C, multiple sclerosis, and others, has resulted in the high demand for generic injectables. This segment covers chemotherapy agents, small molecule antimicrobials, insulin, and peptide hormones, among others.

Distribution Channel Insights

The retail pharmacy distribution channel segment held the highest share of 59.40% in the market in 2022. This can be attributed to the growing burden of chronic diseases in the general population, and the various discounts offered by retail pharmacies. The market has witnessed consolidation in retail pharmacy chains in the U.S.

On the other hand, the hospital pharmacies segment is expected to show moderate growth during the forecast period. Injectable drugs account for a significant proportion of hospital pharmacy sales.

Regional Insights

North America accounted for a revenue share of 20.63% in the global market in 2022 and is expected to advance at a steady CAGR during the forecast period. Moderately high penetration of branded generic drugs and the growing disease burden and geriatric population in the region are among the factors driving growth.

On the other hand, the Asia Pacific market is expected to progress at the highest CAGR of 6.5% during the projection years. The increasing penetration of products in countries such as Japan and India is expected to be a major growth driver. In addition, countries in this region are focusing on the development of their manufacturing hubs to tackle the shortage of life-saving medicines, thus addressing the unmet needs. In countries such as India, doctors prescribe drugs using brand names instead of INN and hence there is a higher demand for branded generics in this region.

Some of the prominent players in the Branded Generics Market include:

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2032. For this study, Nova one advisor, Inc. has segmented the global Branded Generics market.

By Branded Generics Drug Class

By Branded Generics Application

By Branded Generics Route of Administration

By Branded Generics Distribution Channel

By Region

Branded Generics Market