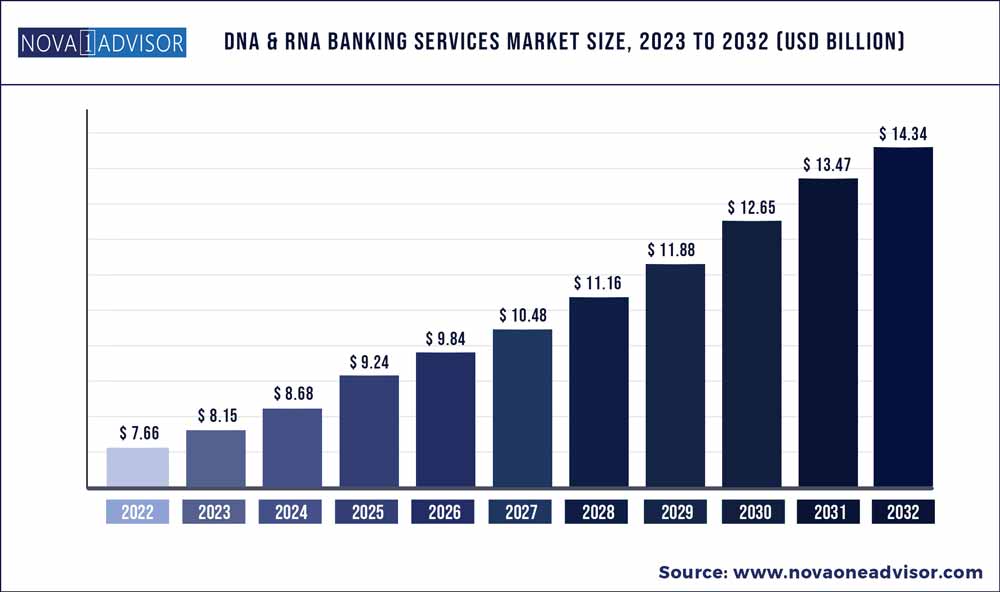

The global DNA & RNA Banking Services market size was exhibited at USD 7.66 billion in 2022 and is projected to hit around USD 14.34 billion by 2032, growing at a CAGR of 6.48% during the forecast period 2023 to 2032.

Key Pointers:

DNA & RNA Banking Services Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 8.15 Billion |

|

Market Size by 2032 |

USD 14.34 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 6.48% |

|

Base year |

2022 |

|

Forecast period |

2023 to 2032 |

|

Segments covered |

Service type, Specimen type, Application, End-use, Region |

|

Regional scope |

North America; Europe; Asia Pacific; Central and South America; the Middle East and Africa |

|

Key companies profiled |

EasyDNA; DNA Genotek Inc.; 23andMe, Inc.; GoodCell; ProteoGenex; US Biolab Corporation, Inc.; Infinity Biologix; Thermo Fisher Scientific, Inc.; deCODE genetics; Brooks Life Sciences; LGC Biosearch Technologies; PreventionGenetics |

Biobanking approaches have been identified as key areas in accelerating the discovery and development of new therapeutic interventions, especially in oncology. This multidisciplinary approach is applied in all aspects of disease prediction, prevention, therapy monitoring, drug discoveries, and optimization. Therefore, a rise in cancer cases globally is expected to drive the demand for DNA and RNA banking services for cancer research. Cancer is the second most common cause of death in the U.S. after heart disease. According to the American Cancer Society estimates, more than 1.8 million new cancer cases were identified by the end of 2020 in the U.S. In addition, approximately 606,520 Americans were estimated to die in 2020 due to cancer. This high prevalence rate of cancer subsequently increases the demand for cancer research, which further accelerates the usage of DNA and RNA banking services.

The emergence of imaging biobanks is one of the recent evolutions where images collected from magnetic resonance, advanced computed tomography, and positron emission tomography are useful in validating and identifying non-invasive biomarkers (IBs). IBs help assess physiological processes and pharmaceutical responses to drugs. Oncologic-oriented imaging biobanks are the most existing types as IBs are used for oncologic purposes, such as tumor volume and glucose metabolism.

Funding and investment programs to expand the DNA and RNA banking approaches globally are expected to boost market growth in the near future. For instance, in July 2019, 54gene, a Nigeria-based startup, raised USD 4.5 million in seed funding for the development of Pan-African Biobank. The company planned to collect 40,000 samples and further expand its collection to gather around 200,000 samples by the end of 2020. This broadened the banking services in emerging nations.

Service Type Insights

Storage service dominated the market with a revenue share of 37.19% in 2022. The acquisition of high-quality biospecimens is vital for researchers. Reliable long-term stabilization and storage of DNA and RNA are critical for the success of biobanks. It is essential to store biological samples in fully qualified, temperature-controlled storage, such as -196 °C; -80 °C; -20 °C; 2.0 °C-8.0 °C; and 15.0 °C-25.0 °C.

The availability of systems, such as comPOUND and arktic systems from SPT Labtech, can be configured for ambient, -20°C and 4°C storage and -80°C solutions, respectively. These platforms are well-suited for a broad range of 2D barcoded sample tubes to fulfill storage volumes ranging from a few microliters to 1.2 mL. Therefore, the presence of solutions for ambient DNA and RNA storage positively impacts segment growth.

Quality control services are anticipated to register the fastest growth rate during the forecast period with the presence of several guidelines to improve the quality and reproducibility of DNA and RNA samples. The Biospecimen Reporting for Improved Study Quality guidelines strengthen the communication and publications related to biospecimen research. On the other hand, France introduced stringent country-specific regulations for banking procedures.

Specimen Type Insights

The blood segment accounted for the largest share of 41.9% in 2022 as it is the most recommended sample type for routine care applications. It is proven to be the most popular specimen type for non-invasive biomarker-based cancer studies. In addition, the time of collecting blood samples does not impact the yield of DNA and RNA.

Though the collection of blood requires certified skills, venipuncture, and special collection tubes, it is a part of routine clinical care. The collection of an additional specimen for storage in biobanks does not burden the patient, thus making blood collection relatively uncomplicated. In addition, serum and plasma are usually preferred over whole blood for cell-free DNA, hormone, and protein as the removed cellular fraction cannot interfere with the results.

Buccal swabs and hair follicle samples are anticipated to expand at a lucrative CAGR over the forecast period. The collection of biological samples from buccal swabs is among the fastest methods and it does not require medically trained personnel. Hair samples are commonly used in forensic studies and usually are not suggested for genetic studies. Moreover, a rise in COVID-19 cases has exponentially increased the demand for swabbing methods for diagnostic testing.

Application Insights

In terms of revenue, drug discovery and clinical research accounted for the largest revenue share of 39.7% in 2022 as DNA and RNA banking services support the scientific progress in the stratification of population and biomarker discovery. These services are important for new drug discovery and clinical research processes. It helps support the entire procedure of patient prevention and prediction, therapy monitoring, follow-up, and therapy optimization.

The paradigm shift toward personalized medicine has further driven the drug discovery and clinical research market. Personalized medicine is based on proteomics, metabolomics, and epigenomics, which involves the usage of DNA and RNA samples for research purposes into new treatments for diseases. These biobanks provide data related to the genotype-phenotype correlations and offer follow-up data to link genetic variation with health outcomes.

DNA and RNA biobanks conduct a wide range of studies for infectious diseases and immunization, which enrolls several hundreds of participants every year. This creates significant opportunities to store DNA and RNA samples for future research on immunity, infectious diseases, and immunization. For instance, the Oxford Vaccine Centre collects DNA and RNA samples to offer data related to immunization and infectious diseases, resulting in the lucrative growth of the therapeutics segment.

End-use Insights

The academic research segment dominated the DNA and RNA banking services market with a revenue share of 35.8% in 2022. The value of DNA and RNA biobanks is well recognized by translational researchers at academic institutions and laboratories. The shifting paradigm toward personalized medicine, tailored therapies, and benefits offered by biomarkers can be attributed to the largest revenue share of the segment. Academic and research centers are involved in understanding the differences between medical treatments and the responses of different individuals.

One such academic institute is the Colorado Center for Personalized Medicine (CCPM) which is engaged in the field of personalized medicine. This center is also a biobank that collects, processes, stores, and tests biological samples. The clinical genetic tests help in the prediction of medications, a carrier for a disease, and the risk of certain diseases.

The hospitals and diagnostic centers segment are expected to witness the fastest growth from 2023 to 2032 with an increase in the number of patients that have consented to provide specimens for hospitals. For instance, over 80,000 patients have consented to provide their biological samples to the Partners Biobank at McLean Hospital, Massachusetts General Hospital, Brigham and Women’s Hospital, and Spaulding Rehabilitation Hospital to date.

Regional Insights

North America dominated the market with a share of 35.4% in 2022. This can be attributed to the presence of several biobanks and continuous efforts undertaken in this region. The Canadian Tumor Repository Network is a non-profit biobanks consortium that is funded by the Government of Canada. The biobank participating in this consortium collects and stores blood, tissue, and saliva samples of cancer patients for several research applications.

The government of the U.S. also supports the comprehensive national biobanking program. The Cooperative Human Tissue Network Biobanks is a non-profit federal organization that is supported by the National Cancer Institute of the U.S. It provides tissues, blood, and tissue microarrays from the existing collection of specimens from cancer patients for specific research projects.

Asia Pacific is projected to register a lucrative growth rate throughout the forecast period. Several conferences and events conducted in this region regarding DNA and RNA banking approaches are among the few factors contributing to the fastest growth of the regional market. For instance, the International Conference on Advanced Biobanking and Biotechnology was hosted in September 2020 in Japan. This conference raised awareness related to DNA and RNA banking in this region.

Some of the prominent players in the DNA & RNA Banking Services Market include:

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2032. For this study, Nova one advisor, Inc. has segmented the global DNA & RNA Banking Services market.

By Service Type

By Specimen Type

By Application

By End-use

By Region

DNA & RNA Banking Services Market