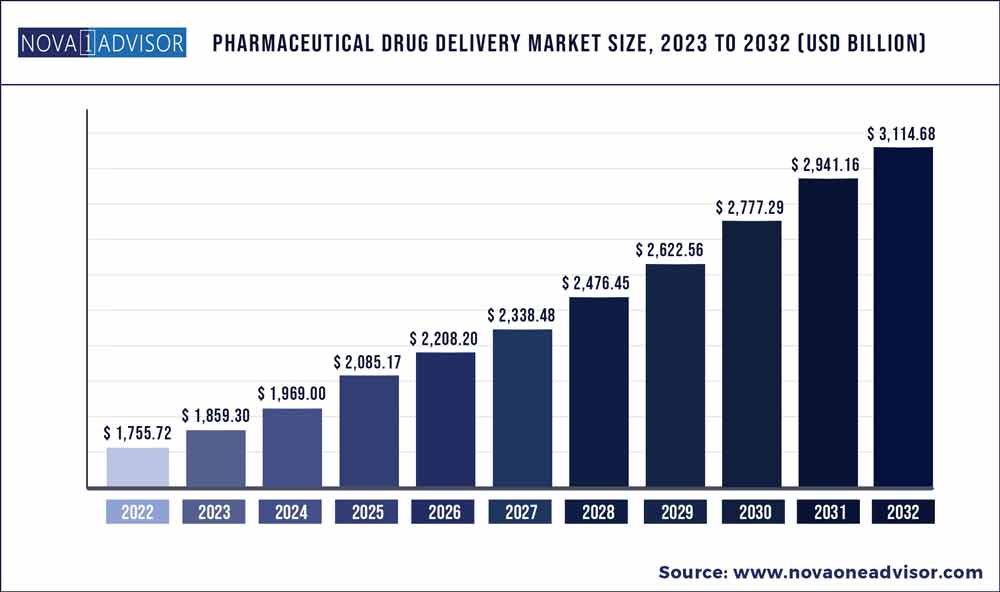

The global pharmaceutical drug delivery market size was exhibited at USD 1,755.72 billion in 2022 and is projected to hit around USD 3,114.68 billion by 2032, growing at a CAGR of 5.9% during the forecast period 2023 to 2032.

Key Pointers:

Growth in the pharmaceutical drug delivery market can largely be attributed to factors such as the rising prevalence of chronic diseases, the growing biologics market, increasing R&D investments, technological advancements, and new product launches. Moreover, pharmaceutical and biopharmaceutical companies are focusing on R&D to develop new molecules for various therapeutic applications and drug delivery platforms. The companies invest heavily in R&D with the aim of delivering high-quality and innovative products to the market. R&D spending by biopharmaceutical companies has also increased over the years. On the other hand, the risk of needlestick injuries and the increased pricing pressure are expected to limit the market's growth to some extent in the coming years.

Pharmaceutical Drug Delivery Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 1,859.30 billion |

|

Market Size by 2032 |

USD 3,114.68 billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 5.9% |

|

Base year |

2022 |

|

Forecast period |

2023 to 2032 |

|

Segments covered |

Route of Administration, Application, Facility of Use |

|

Regional scope |

North America; Europe; Asia Pacific; Central and South America; the Middle East and Africa |

|

Key companies profiled |

Johnson & Johnson (US), Novartis International AG (Switzerland), F. Hoffmann-La Roche AG (Switzerland), Pfizer Inc. (US), Bayer AG (Germany), Antares Pharma, Inc. (US), Becton, Dickinson and Company (US), GlaxoSmithKline plc (UK), 3M (US), Merck & Co., Inc. (US), Sanofi (France), Amgen, Inc. (US), AbbVie Inc. (US), Genmab A/S (Denmark), Gilead Sciences, Inc. (US), Boehringer Ingelheim (Germany), AstraZeneca plc. (UK), Eli Lilly and Company (US), Teva Pharmaceuticals Industries Ltd. (Israel), Bristol-Myers Squibb (US), Gerresheimer AG (Germany), Boston Scientific Corporation (US), Nimbus Therapeutics (US), Kite Pharma (US), and IDEAYA Biosciences, Inc. (US). |

Pharmaceutical Drug Delivery Market Dynamics

Drivers: Growth in biologics market

Recognizing the potential for biologics manufacturing, companies, such as Evonik (Germany), have made several strategic developments. For instance, the company increased its production capacity by acquiring SurModics in 2022, which focuses on controlled-release parenteral applications. In addition, Evonik acquired complementary technologies, such as Boehringer Ingelheim’s RESOMER platform, to improve its capability in this market. Similarly, in 2019, WuXi Biologics announced the launch of WuXi Vaccines, a joint venture with Shanghai Hile Bio-Technology Co., Ltd. The companies entered into a strategic partnership under which WuXi Vaccines will build a dedicated facility and supply a commercial product for the global market. The biopharmaceutical industry has witnessed the emergence of a new class of therapeutics, showing significant potential for new treatments in oncology, diabetes, and other disease areas.

Restraints: Risk of needlestick injuries

Needlestick injuries are one of the most serious health and safety threats:

Opportunities: Self-administration and home care

Self-administration and home care are expected to provide significant growth opportunities for players operating in the pharmaceutical drug delivery market. This is mainly due to the rising geriatric population, as elderly individuals form a large consumer base for drug delivery devices for home care. This factor is also increasing the need for application-specific injection, inhalation, topical, and transdermal drug products that are designed to cater to the needs of caregivers and patients.

Challenges: Pricing pressure

Government bodies in both developed and developing countries are encouraging cost-saving measures, such as cutting drug reimbursement prices and promoting the greater use of generics. Drug manufacturers across the globe are facing significant cost reduction pressures from government bodies, insurers, and patients. This downward pricing pressure is resulting in a greater uptake of drugs in emerging markets, where the demand for low-cost therapeutics is high. However, this is affecting the profitability of several pharmaceutical companies. This trend is expected to continue in the coming years due to ongoing pressure from insurers, pharmacy benefit managers (PBMs), and public and private payers to reduce pharmaceutical prices due to concerns about covering more new medicines to treat common conditions such as high cholesterol and diabetes.

The topical drug delivery segment is expected to grow at the highest CAGR during the forecast period

Based on the route of administration, the pharmaceutical drug delivery market is segmented into oral, pulmonary, injectable, ocular, nasal, topical, implantable, and transmucosal drug delivery. The topical drug delivery segment is expected to grow at the highest CAGR during the forecast period from 2023 to 2032. This can be attributed to convenience and ease of use, the ease of dosage, painless and non-invasive administration, and enhanced patient compliance.

In 2022, the infectious disease segment accounted for the largest share of the market

On the basis of application, the pharmaceutical drug delivery market is segmented into cancer, infectious diseases, cardiovascular diseases, diabetes, respiratory diseases, central nervous system disorders, autoimmune diseases, and other applications. In 2022, the infectious diseases segment accounted for the largest share of the global market. The large share of this market segment can be attributed to the increasing prevalence of infectious diseases across the globe, increasing R&D expenditure for new drugs owing to the current COVID-19 pandemic scenario, and the rising number of FDA approvals for such drugs.

The home care settings segment is expected to grow at the highest CAGR during the forecast period

Based on the facility of use, the pharmaceutical drug delivery market is segmented into hospitals, ambulatory surgery centers (ASCs) or clinics, home care settings, diagnostic centers, and other facilities of use. The home care settings segment is projected to grow at the highest CAGR during the forecast period. Growth in this segment can be attributed to the increasing use of drug delivery devices, such as injectables, nebulizers, and inhalers, in home care settings. Topical drug delivery systems are also increasingly gaining prominence, not just as an alternative route of drug delivery but also as point-of-care devices in in-home care settings.

Region Insights

Based on region, North America dominated the global market in 2022. This is attributed to the increased prevalence chronic diseases among the US population. According to a study, around 60% of the US population is suffering from at least one chronic diseases and most of them are affected with more than one disease. Moreover, the development of various innovative drugs in the biopharmaceutical industry that can treat various non-communicable diseases is exponentially fueling the demand for the pharmaceutical drug delivery solutions in North America. Furthermore, the rising demand for the personalized drugs in North America is impacting the market positively.

Asia Pacific is estimated to be the most opportunistic market during the forecast period. This is attributed to the rising prevalence of various chronic diseases among the population owing to various factors such as physical inactivity, sedentary lifestyle, and unhealthy food habits. The rapidly growing biotechnology and rising demand for the biotechnology drugs in the region is spurring the demand for the pharmaceutical drug delivery. According to the World Health Organization, maximum number of deaths due to the chronic diseases is recorded in the low and middle income countries. Therefore, the rising accessibility to the healthcare facilities is prominently driving the market growth in this region.

Some of the prominent players in the Pharmaceutical Drug Delivery Market include:

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2032. For this study, Nova one advisor, Inc. has segmented the global Pharmaceutical Drug Delivery market.

By Route of Administration

By Application

By Facility of Use

By Region

Pharmaceutical Drug Delivery Market