Prostate Cancer Therapeutics Market Size, Share & Analysis Report, 2023-2032

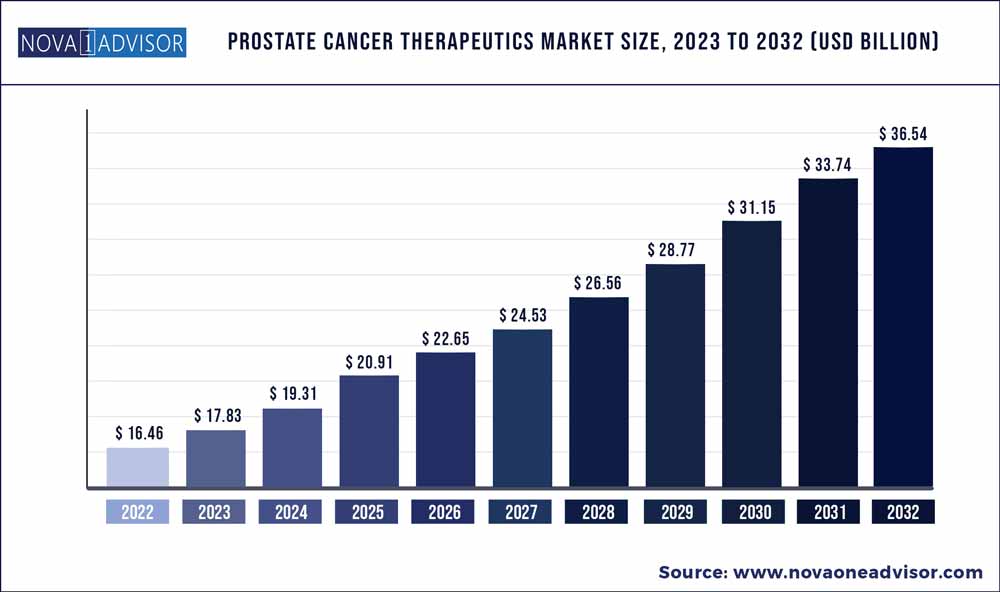

The global Prostate Cancer Therapeutics market size was exhibited at USD 16.46 billion in 2022 and is projected to hit around USD 36.54 billion by 2032, growing at a CAGR of 8.3% during the forecast period 2023 to 2032.

Key Pointers:

Prostate Cancer Therapeutics Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 17.83 Billion |

|

Market Size by 2032 |

USD 36.54 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 8.3% |

|

Base year |

2022 |

|

Forecast period |

2023 to 2032 |

|

Segments covered |

Drug class, Distribution channel, Region |

|

Regional scope |

North America; Europe; Asia Pacific; Central and South America; the Middle East and Africa |

|

Key companies profiled |

Johnson & Johnson; Services Inc.; Astellas Pharma Inc.; Eli Lilly and Company; Sanofi; Ipsen Pharma; Bayer AG; AstraZeneca; Valeant Pharmaceuticals International, Inc.; Merck & Co., Inc.; Pfizer Inc. |

The market is witnessing growth due to the factors such as the increasing prevalence of prostate cancer, the adoption of novel screening and diagnostic technologies, and government support for new therapies to cure prostate cancer. The adoption of novel screening and diagnostic technologies is projected to promote the adoption of therapeutics. Recent breakthroughs in therapies use bioinformatics and computational biology technologies to obtain optimal treatment. Market players have discovered successful techniques for developing new cures and treatments with a focused strategy that includes proteome profiling, exome sequencing, and whole-genome sequencing. For instance, in 2022, over 4,000 men are going under phase III trial for Olaparib where tumor genomic testing was used as a means of identification of patients.

The global pandemic has had a significant impact on a number of aspects of cancer care, including doctor-patient relationships, access to therapy, and physicians therapeutic choices, in addition to having a wide range of social, economic, and sanitary consequences that have exacerbated pre-existing threats to public health, such as those related to pollution. This has ultimately had a negative impact on mortality from cancer. In contrast, COVID-19 is linked to higher mortality rates in cancer patients as compared to non-cancer patients.

Major players operating in the market are focusing on developing novel and advanced products. Many companies have products in their product pipeline which are expected to be launched in the market during the forecast period. For instance, in March 2022, Merck announced keylynk-010 a trial for evaluating keytruda in combination with lynparza in patients with metastatic castration-resistant prostate cancer.

Government support for new therapies to cure prostate cancer is propelling market growth. For instance, in March 2022, US FDA approved 177Lu-PSMA-617, a new metastatic prostate cancer treatment. The Society of Nuclear Medicine and Molecular Imaging developed this new therapy showing to reduce the risk of death by 38 percent. This new treatment is based on the use of PET scans to identify and treat patients with metastatic prostate cancer that express PSMA (prostate-specific membrane antigen).

Targeted therapy comes at a high price, which makes them unaffordable to the general public. For instance, the American Society of Clinical Oncology published a report in May 2021, concluding that the U.S. has the highest cancer medicine prices, which are more than two times higher than in Europe and two to six times higher than the rest of the globe.

Drug Class Insights

Hormonal therapy drug class segment dominated the market in 2022 with a revenue share of 89.34% in 2022. The hormonal therapy includes drugs majorly acting as luteinizing hormone-releasing hormone (LHRH) antagonists, luteinizing hormone-releasing hormone (LHRH) antagonists, and anti-androgen. One of the most commonly used drugs is Xtandi, and not just because more patients are receiving prostate cancer treatment, but because more patients are taking it for longer durations, the average duration is now nine months. The drug generated a revenue of over 3 billion in 2021. The trend is expected to continue as more urologists continue to recommend the therapy, which helps Xtandi's revenue stream over the long term.

Chemotherapy drug class is expected to grow at a lucrative growth rate over the forecast period attributable to the presence of drugs Taxotere and Jevtana. Chemotherapy is generally used in patients when prostate cancer is spread outside the prostate and hormonal therapy is inefficient in the treatment of the diseased condition. Jevtana drug has the highest revenue share in the chemotherapy drug class this can be attributed to the ability of the drug to reduce the risk of death by 36%.

Immunotherapy is projected to demonstrate a positive growth trend over the forecast period. Provenge is the only product with FDA approval in the segment. It is first of its kind preventive prostate cancer vaccine. The pipeline for prostate cancer demonstrates a strong potential with ongoing gene therapy, stem cell therapy, small molecules, and vaccine trials.

Distribution Channel

The hospital pharmacies segment dominated the market and accounted for the largest revenue share in 2022. Hospital pharmacies and pharmacists are important market participants because they manage pharmaceuticals in a critical hospital setting that necessitates quick access to drugs and supplies. Additionally, these pharmacies provide both in-patient and out-patient services, making it simple for patients to treat a wide variety of illnesses. Moreover, these pharmacies also strive to lower clinical decision-making errors and concentrate on generating income from medicine purchases while aiming to lower the overall cost of prescriptions.

In August 2022, Royal Surrey became the first to introduce Lutetium 177 treatment for prostate cancer patients under the Early Access Medicine Scheme (EAMS). The move has been taken post the marketing authorization grant for the product by The Medicines and Healthcare Products Regulatory Agency (MHRA). The use of nuclear medicine requires special assistance, thereby, enhancing the role of hospitals.

Online pharmacies are expected to witness a lucrative growth rate over the forecast period attributable to easier access to the internet and increasing awareness among people about over-the-counter medicines, online pharmacies have gained popularity quickly. Additionally, COVID-19 has positively impacted the sector, propelling the market at an exponential rate, which is related to the constraints on people's freedom of movement. Moreover, the growth of the market is also linked to e-prescriptions, and as this trend gains traction, it could help the situation with online pharmacies.

Regional Insights

North America dominated the prostate cancer therapeutics market and accounted for the largest revenue share of 42.3% in 2022, due to an increase in the disease's prevalence, and a strong need for prostate cancer therapeutic products in the region. However, the advent of promising new medicines in the biologics and hormone therapy divisions is attributable to expansion in North America. During the projection period, the planned introduction of some pipeline drugs is predicted to drive the market in the area. For instance, In March 2022, US FDA approved an advanced accelerator application for Pluvicto drug, which will be used to treat adult patients with prostate cancer. The presence of a strong pipeline and government support for the innovation is anticipated to drive the market over the forecast period.

Asia Pacific region is estimated to demonstrate the fastest growth over the forecast period. The growth of the market is attributed to cost-effective treatment, tailored medicines, technological advancements, the availability of numerous treatment options, and the rising incidence of prostate cancers. For instance, Xtandi (enzalutamide), which is co-licensed by Astellas Pharma of Japan and Pfizer of the United States, for the treatment of men with prostate cancer and is priced five times cheaper than compared the U.S. Such cost-effective treatment and technological advancements in the market are expected to boost the market growth over the forecast period.

Some of the prominent players in the Prostate Cancer Therapeutics Market include:

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2032. For this study, Nova one advisor, Inc. has segmented the global Prostate Cancer Therapeutics market.

By Drug Class

By Distribution Channel

By Region