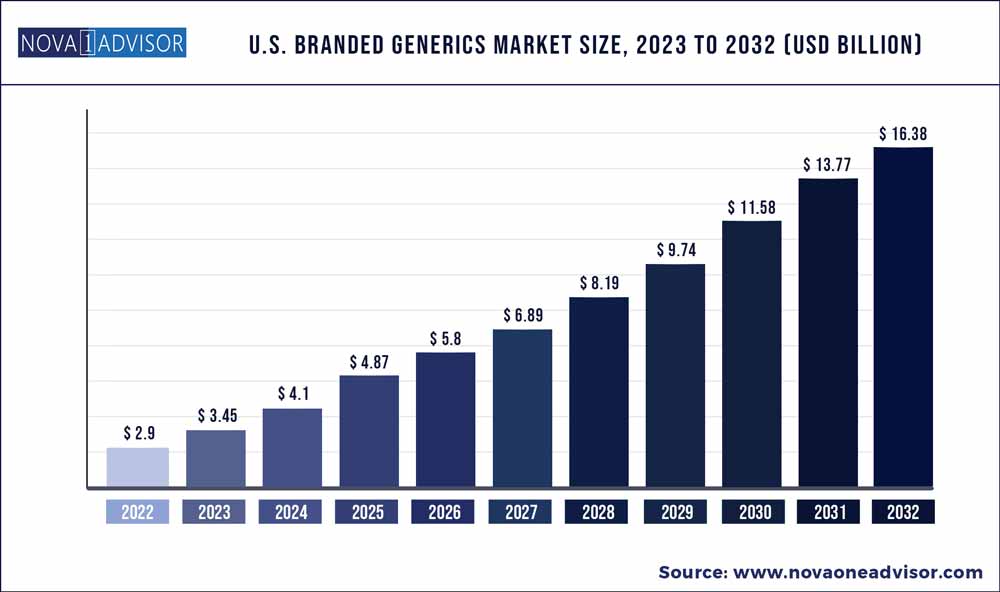

The US branded generics market size was exhibited at USD 2.9 billion in 2022 and is projected to hit around USD 16.38 billion by 2032, growing at a CAGR of 18.9% during the forecast period 2023 to 2032.

Key Pointers:

Report Scope of the US Branded Generics Market

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 3.45 Billion |

|

Market Size by 2032 |

USD 16.38 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 18.9% |

|

Base Year |

2022 |

|

Forecast Period |

2023 to 2032 |

|

Segments Covered |

Drug class, application, route of administration, distribution channel |

|

Key companies profiled |

Amneal Pharmaceuticals LLC, Apotex Inc., AstraZeneca PLC, Aurobindo Pharma Limited, Bausch Health Companies Inc., Cipla Limited, Dr. Reddy’s Laboratories Ltd., Endo International PLC, Eris Lifesciences Limited, Eva Pharma, Fresenius Kabi AG, GlaxoSmithKline PLC, Glenmark Pharmaceuticals Limited, Hetero Drugs Limited, Lupin Pharmaceuticals, Inc., and Mylan N.V.. |

The Factors such as patent expiry of major products, the rising prevalence of chronic diseases, high penetration of generic products, and government initiatives to promote them for reducing the overall healthcare expenditure are among the primary growth drivers.

The patent expiry of branded products primarily fuels industry growth. Drugs, such as Revlimid and Alimta, may cost up to USD 500 a month, which affects the overall healthcare expenditure and affordability for patients suffering from chronic diseases. Eli Lilly & Company’s Alimta is expected to lose its patent protection by May 2022. This expiry of product patents creates opportunities for generics and biosimilar manufacturers.

However, over the past few years, the trend of ANDA approvals for generic drugs had been steadily decreased. It can be observed that the number of ANDA approvals decreased from 1,014 in 2019 to 948 in 2020 and further declined to 776 in 2021. Such factors could slow down industry growth in the coming years.

The growing burden of infectious & non-infectious diseases, coupled with the rising geriatric population, which is more susceptible to chronic diseases such as diabetes, hypertension, and obesity, is expected to positively impact the industry growth. According to an NCBI article, there were 537 million patients suffering from diabetes in 2021 globally.

The COVID-19 pandemic moderately impacted the branded generics space. Due to lockdown situations and stringent government regulations to curb the pandemic, a slowdown and disruption in the supply of pharmaceuticals had been observed in the initial phase of the pandemic. In addition, regulatory operations also affected reimbursement decisions and approvals of new products in the space. However, the market regained its pace by the end of 2020 in most countries.

Companies are introducing novel products to strengthen their product portfolio. In March 2022, Viatris, Inc. received the U.S. FDA’s approval for Breyna, the first generic version of AstraZeneca's Symbicort, intended for the treatment of COPD. Moreover, in February 2019, Mylan N.V. introduced the first generic version of ADVAIR DISKUS (fluticasone propionate and salmeterol inhalation powder) under the brand Wixela Inhub for the treatment of patients with Chronic Obstructive Pulmonary Disease (COPD) or asthma. This branded generic was claimed to be 70% cheaper than the originator product.

US Branded Generics Market Segmentation

| By Drug Class | By Application | By Route of Administration | By Distribution Channel |

|

Alkylating Agents Antimetabolites Hormones Anti-hypertensive Lipid Lowering Drugs Anti-depressants Anti-psychotics Anti-Epileptics Others |

Oncology Cardiovascular Diseases Neurological Diseases Gastrointestinal Diseases Dermatological Diseases Acute And Chronic Pain Others |

Topical Oral Parenteral Others |

Hospital Pharmacy Retail Pharmacy Online Pharmacy |

U.S. Branded Generics Market