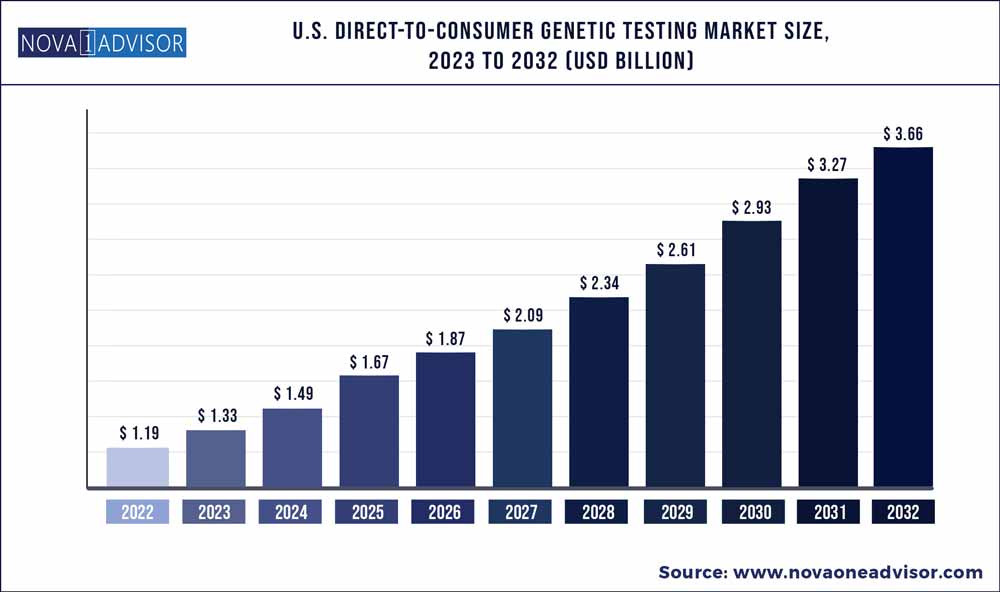

The U.S. direct-to-consumer genetic testing market size was exhibited at USD 1.19 billion in 2022 and is projected to hit around USD 3.66 billion by 2032, growing at a CAGR of 11.9% during the forecast period 2023 to 2032.

Key Pointers:

Report Scope of the U.S. Direct-to-Consumer Genetic Testing Market

|

Report Coverage |

Details |

|

Market Size in 2023 |

USD 1.33 Billion |

|

Market Size by 2032 |

USD 3.66 Billion |

|

Growth Rate from 2023 to 2032 |

CAGR of 11.9% |

|

Base Year |

2022 |

|

Forecast Period |

2023 to 2032 |

|

Segments Covered |

Test Type, Technology and Distribution Channel |

|

Key companies profiled |

Ancestry, Easy DNA, 23andMe, Inc., HomeDNA, Counsyl, Living DNA Ltd., and Pathway genomics, among others. |

Growing incidence of genetic diseases such as breast cancer, colon cancer, and achondroplasia is likely to increase the demand for DTC tests. As per US CDC, nearly 264,000 cases of breast cancer are diagnosed in women, and around 2,400 in men, annually in the US. Another estimate from the American Cancer Society Data suggests that the country reported 106,180 new cases of colon cancer in 2022. This has elevated the demand for high-quality DTC genetic tests, that are capable of diagnosing genetic disorders much earlier, which has effectively decreased mortality rates among cancer patients, augmenting industry expansion.

Defective DTC genetic tests may pose a major challenge to the U.S. direct-to-consumer genetic testing market by stifling demand for these test kits. A study by Ambry Genetics, a leading genetic tests company, found that these tests may yield 40% false positive results. A higher ratio of incorrect results directly impacts the demand for DTC tests as healthcare providers are growing more cautious about putting patient health at stake. Privacy concerns are also likely to hold back growth as the genome sequencing data obtained through these tests can be released into the public, with companies utilizing it for other purposes.

With respect to test, the U.S. DTC genetic testing market share from predictive testing segment is poised to grow at a 13.7% CAGR through 2023 to 2032. The increasing incidence rate of chronic and genetic diseases in the region is likely to drive the segment progression. The disease load of inherited ailments such as cystic fibrosis, sickle cell anemia, thalassemia, and hemophilia in growing at a rapid pace in the U.S., creating a higher growth impetus for the DTC test sector.

On the basis of technology, the U.S. direct-to-consumer genetic testing market share from the single nucleotide polymorphism (SNP) chips segment is poised to grow at over 11.9% CAGR from 2023 to 2032. Substantial usage of single nucleotide polymorphism (SNP) chips in genome sequencing is expected to drive the segment revenues. These chips study gene sequences at a particular resolution and present a detailed analysis of the defective genes that may cause certain disorders in the future. The SNP technology is capable of analysing changes in a single letter, which boosts the efficiency of tests. In fact, SNP chips used for the diagnosis of hereditary cancers have detected 1300 mutations in BRCA2 genes.

Based on distribution channel, the U.S. DTC genetic testing market size from online platforms was valued at over USD 1.8 billion in 2022, driven by increasing consumer preference for online shopping and the popularity of tests such as 23andme and ancestry. Meanwhile, rising healthcare investments in the region is also fostering the market outlook.

With increasing per capita income and rising consumer awareness, leading players in the field are focusing on consolidating a presence on e-commerce and online retail platforms to make their products more easily accessible to customers.

U.S. Direct-to-Consumer Genetic Testing Market Segmentation

| By Test Type | By Technology | By Distribution Channel |

|

Carrier testing Predictive testing Ancestry & Relationship Testing Nutrigenomics Testing Skincare Testing Others |

Targeted analysis Single nucleotide polymorphism (SNP) chips Whole genome sequencing [WGS] |

Online platforms Over-the-Counter |

U.S. Direct-to-Consumer Genetic Testing Market